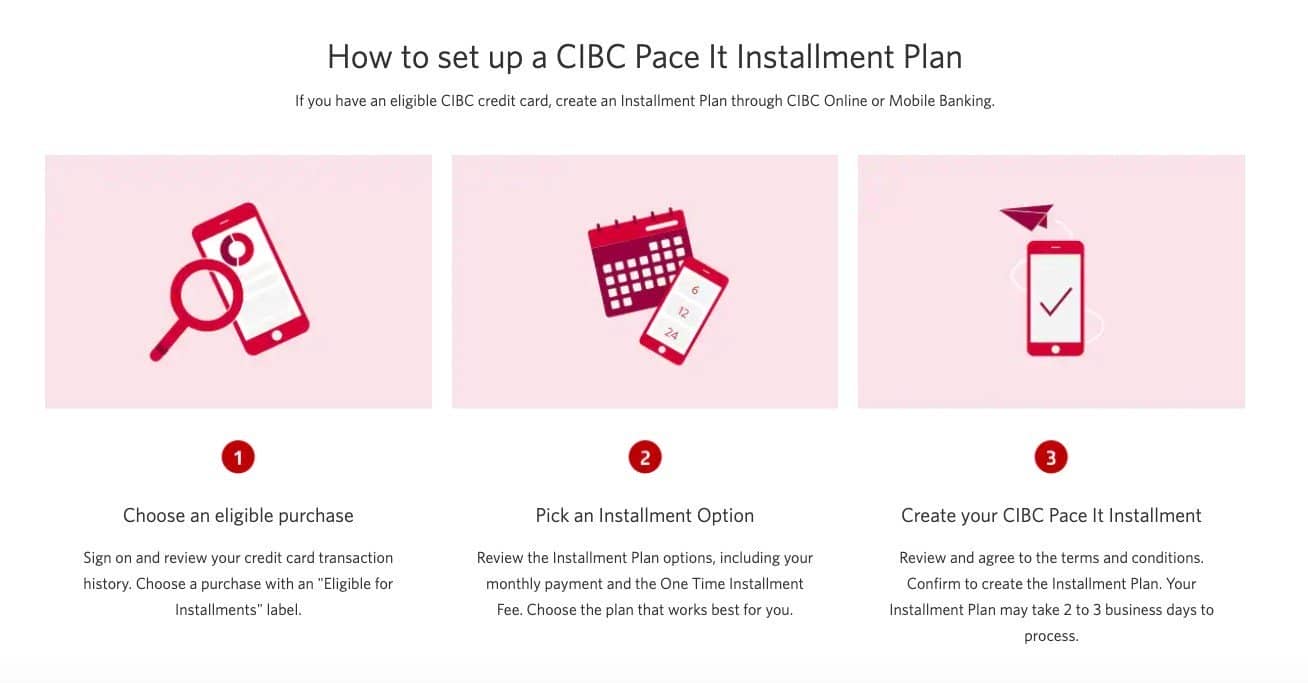

In this article let us take a look at everything CIBC Pace It has to offer. But, before we get started, what exactly is “CIBC’s Pace It”? How Do You Convert your purchases into installments? Is it really beneficial in the long run saving credit card interest charges? Let’s find that out in this article.

Let us first begin by looking at the basics – What Is CIBC Pace It?

What Is CIBC Pace It?

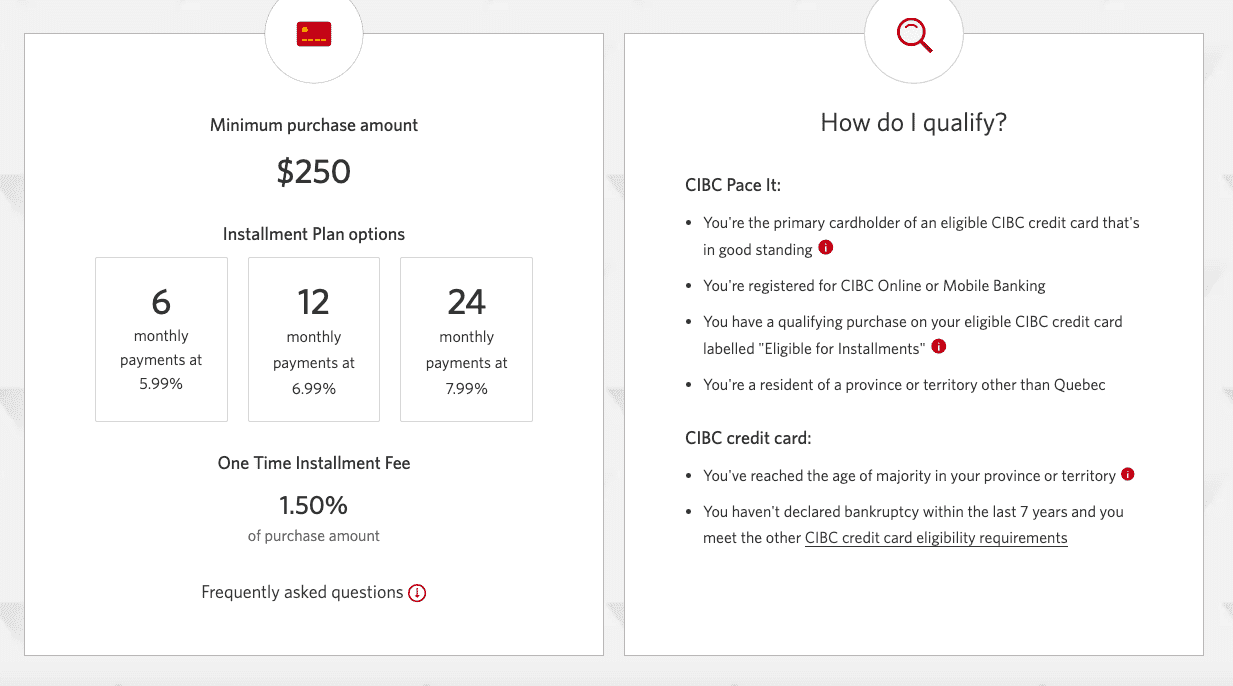

Every purchase you make using your CIBC credit card is eligible to convert to an installment plan. The minimum purchase amount should be above $250.

CIBC charges a fee of 1.5% of each purchase you set up on an Installment Plan. Fees are subject to the Interest Rate for Purchases (19.99%). When you make your Credit Card Payments, what Banks do is categorize your purchases and then prorate your payment when applying it to the account. This is to ensure that you pay the most interest possible.

Usually, In Canada, all the major credit card companies charge a 19.99% interest for regular purchases and 22.99% for cash advances. That’s where Pace It comes in, you’ll save money on interest by converting all eligible purchases into installments over a 6,12 or 24-month installment plan. The interest rates are applicable once the grace period expires.

Now, let us look at the real world scenario of using the CIBC Pace It program. It’ll help you understand the benefits better.

What Is The Fee Associated With CIBC Pace It?

Every time you set up a new Installment Plan, there’s a One Time Installment Fee that’s 1.50% of the purchase amount you converted. You pay the One Time Installment Fee in the first monthly credit card statement after you’ve created the Installment Plan. The fee will be included in your minimum payment and also part of your total balance.

Example:

If you set up a CIBC Pace It Installment Plan on a $900 purchase of a new couch, the One Time Installment Fee will be $13.50 (1.50% of $900).

CIBC Pace It – Real Life Case Scenario

Example: I use Pace It to Finance a $10,000 purchase over 24 months. There is a fee of $150 for setting up the Installment Plan

The $10,000 Purchase has an interest rate of 7.99% (for 24 months)

The $150 Fee has an interest rate of 19.99%

Total Balance on my Credit Card is $10,150. 98.5% is the Installment Plan. 1.5% is the Fee.

I have some extra cash this month and make a payment of $600 on the Credit Card.

$600 * 98.5/100 = $591.00 This is applied to the Installment Plan.

$600 * 1.5/100 = $9.00 This is applied to the Fee.

As you can see from my example, the Bank is applying the majority of the payment to the portion of the balance with the lower interest rate. The only way to stop paying 19.99% interest on the Fee is to pay your account in full….also, obviously, if one chooses to Finance using the Credit Card, you lose your Interest-Free Grace Period.

Notice how this is not offered in Quebec….because Quebec has stronger Consumer Protection Laws, and this type of arrangement is forbidden. CIBC even explicitly states that anybody who sets up Installment Plans under Pace It, and then becomes a resident of Quebec will have those Installment Plans cancelled.

Examples of the 6, 12, and 24 Month Installment Plan Payments

When you make an eligible purchase of $250 or higher, you will see the “Eligible for Installments”, option in the transaction history. After you pick an installment plan option (6, 12, or 24 months), the one-time 1.5 percent fee is then applied.

Let’s say you make an eligible purchase totalling $300, here’s the installment plan breakdown:

6 payments at 5.99 percent

Your monthly payment is about $50.88 and there’s a $4.50 installment fee.

The $300 purchase is now $309.78.

With a 19.99 percent interest rate, you would pay $317.74 for this purchase, that’s $7.96 more interest.

12 payments at 6.99 percent

Your 12 monthly payments are about $25.96 each, and there’s a $4.50 installment fee.

The $300 purchase is now $316.02.

At a 19.99 percent interest rate, you would pay $17.48 more in interest.

24 payments at 7.99 percent

Your monthly payment is about $13.57, and there’s a $4.50 installment fee.

The $300 purchase is now $330.18.

Under the standard 19.99 percent interest rate, you would pay $36.31 more in interest than you would with the Pace It

How Does CIBC Pace It Affect My Available Credit?

Using CIBC Pace It doesn’t change your available credit. The original purchase amount is automatically deducted from your available credit. As you pay off your monthly installments, the amount you pay off is added back to your available credit.

Example:

Your credit limit: $5,000. Purchase converted to Installment Plan: $900 for a new couch

Installment Plan selected: 6-months at 5.99%

One Time Installment Fee: 1.50% of the transaction ($13.50)

Available credit: Credit limit [$5,000] – Transaction total [$900] – One Time Installment Fee [$13.50] = $4,086.50

Pace It Plan Benefits and Features

The Pace It installment plan is available through most of the CIBC credit cards for personal accounts. And, customers can choose to select their regular credit card option or the Pace It installment plan for any qualifying purchases.

According to Edward Penner, CIBC’s Executive Vice-President, CIBC understands that Canadians might have large and unplanned purchases. The Pace It plan gives credit cardholders more flexibility as they can select their payment terms and interest rate.

CIBC Pace It Plan Benefits

1. Customers can choose the payment terms and interest rate they want

2. Customers still have the benefit of rewards privileges and insurance through their credit card

Any purchases will be based on current credit scores/approval so customers don’t have to reapply for credit

3. Customers have fast digital access to the installment plan through their mobile device

The installment plan terms will show on the monthly billing statement.

How Does CIBC Apply Payments To Its Credit Cards?

a) When we receive a payment, we first apply the payment to your Minimum Payment in the following order: billed interest (excluding interest for Installment Plans); 2. Installment Plan payments (including interest) due on that statement; 3. billed fees; 4. billed Transactions; 5. unbilled fees; 6. unbilled Transactions

b) If we receive more than your Minimum Payment, we apply the rest of your payment to your remaining Amount Due as follows:

First, we divide the rest of your Amount Due into different groups. All items within a group will have the same interest rate. For example, all Purchases at 19.99% interest will be put in one group, and all Balance Transfers at 0% interest will be put in a different group, etc.

Second, we allocate the rest of your payment to each group based on the percentage that each group makes up of your remaining Amount Due. For example, if 80% of your remaining Amount Due is made up of Purchases at 19.99%, we will allocate 80% of the rest of your payment to this group.

c) If we receive a payment that is more than your Amount Due, we apply the rest of your payment in the following order: unbilled Transactions, using a method consistent with Section 9(b) above

Installment Plan payments that are not yet due, using a method consistent with Section 9(b) above

Credit balances are applied to unbilled items in the order they are posted to your Account.

d) If you accept a special offer that provides for a different way of applying for your payments, the terms and conditions of that offer will apply.

CIBC will always apply Minimum Payments to the Installment Plan first before the Fees; and will always apply the majority of any additional payment to the Installment Plan.

What if I return a purchase that I’ve converted into an Installment Plan?

If you return a purchase that you’ve converted into an Installment Plan, you’ll receive a credit for the return in your account. The credit gets applied to the overall balance in your account, not the Installment Plan. Your Installment Plan will continue as scheduled. If you no longer want your Installment Plan, cancel it through online or mobile banking.

If your return credit is less than your current credit card balance, your Installment Plan won’t be cancelled. If you no longer want your Installment Plan, cancel your Installment Plan through online or mobile banking.

When do I make my monthly Installment Plan payments?

Make your monthly Installment Plan payments when they show up on your next credit card statement after you created the Installment Plan. The monthly Installment Plan payment appears on your credit card statement as part of the minimum payment due and amount due.

Can I change my Installment Plan once I’ve set it up?

No, you can’t change an Installment Plan once you set it up, but you can cancel it any time.

What happens to my Installment Plan if I cancel my CIBC credit card?

If you cancel your CIBC credit card with Installment Plans, you also cancel the Installment Plans. The unpaid Installment Plan balance reverts back to the annual interest rate of your cancelled credit card. You need to pay the full credit card balance in order to pay your Installment Plans in full.

How will using CIBC Pace It affect my CIBC Payment Protector Insurance premiums?

If your credit card is insured with CIBC Payment Protector Insurance for Credit Cards, the premium will be calculated in the same way as before you set up your Installment Plan.

The premium will also be charged on the 1.50% Installment Plan set-up fee since it is part of the Total Balance.

Can I combine multiple purchases into one Installment Plan?

No, you can’t combine multiple purchases into one Installment Plan. You need to create a new Installment Plan for each eligible purchase.

Where can I review my Installment Plan details?

After you create your Installment Plan, it may take 2 to 3 business days before you see your Installment Plan details. Access your Installment Plan details by signing on to online or mobile banking and selecting the “CIBC Pace It Installments” tab. Your Installment Plan details are also available on your monthly credit card statement.

CIBC Pace It Vs. Other Alternatives

Triangle card gives you interest-free instalments for Canadian Tire. Not the same…but at least it’s interest-free.

Brim also has something like this, but they do charge a fee for it even though they make a claim it’s interest-free, which I think is the kind of being deceitful with their marketing. At least CIBC is being upfront and honest about it.

Conclusion

There you go, in a nutshell, CIBC Pace It is a good program overall, you will definitely save on the interest fees by converting your purchases to a 6, 12 or 24-month installment plan.

But do consider your options before converting as your credit limit available will be blocked for the period your installment plan is active. Also, you will end up paying a one-time installment fee.

There’s no cap on the number of installments you can have. You may have as many active installments as possible.

Please share this article if you found it helpful. Also, let me know your thoughts and comments below.

Top 10 Popular Posts Of All Time

- Top 30 Canadian Blue Chip Stocks You Should Own

- How To Use A My Service Canada Account

- Top 7 Personal Finance Apps You Should Install In Canada

- How To Watch Free TV Shows In Canada – List of 10 Best Sites

- 10 Costco Membership Benefits You Need To Know Today

- How To Open A CRA My Account – Helpful Step-By-Step Guide

- Retirement Benefits & Old Age Security Pension (OAS) In Canada

- 7 Quick Ways To Maximize Your PC Optimum Points

- WestJet Rewards Review – Everything You Need To Know

- How To Get An Emergency Canadian Passport – Complete Guide