With the help of a premium service like WealthBar, you can get a professionally managed portfolio in minutes. While brokerages have gotten more innovative with names like Questrade offering a hybrid service catering to both self-directed traders and Couch Potato investors, WealthBar was designed strictly for passive investors.

Here’s what WealthBar’s Homepage quotes – “Whether you’ve got $1,000 or $1 million, we make accessing professionally managed investments and financial advice ridiculously easy.” Apparently, everyone else wants to make money via trading, but not everyone has the requisite know-how to make it happen. This is the primary reason why Robo-advisors exist: to enable those who are short of investment and trading knowledge, expertise, time, and budget to get a piece of the pie too.

In recent years, online brokerages seem to be the major way people want to go when investing and trading with their money.

WealthBar Introduction

Wealthbar, Canada’s first Robo-advisor, is a financial investment management platform created for people who don’t have the financial capacity to invest in exorbitant portfolios. The platform was created sometime in the year 2013 by Chris Nicola and Tea. These two tech-savvy financial investment experts saw the need to create a simpler and faster channel to invest in portfolios in Canada since the available alternatives were either expensive or beyond the reach of the common folks.

In the past, investing in certain financial assets and securing professional investment advice for stock portfolios were restricted to people whose financial capacity was well above the thousand-dollar range or well within the million-dollar range.

Albeit a third choice exists (mutual funds) for people incapable of investing huge capital in a stock portfolio; that too comes with an exorbitant price tag. Wedged between two equally expensive financial investment plans, investors are left with no choice but to depend on do-it-yourself investment management alternatives. This is where Robo-advisors like Wealthbar shine brightly.

Why Choose WealthBar?

Wealthbar is an internet-based financial technology service provider. it is the first-ever online portfolio management company to ever emerge out of Canada, and it has pioneered several other fin-tech platforms in Canada and beyond.

Even though it started with two creative geniuses, Tea and Chris Nicola, Wealthbar has transcended from a small internet-based investment advisor to become one of the biggest across the world. In 2018, this investment portfolio management platform pulled in over 250 million dollars in assets. This is besides the long list of accomplishments they’ve had in asset management and professional investment advice.

Presently, Wealthbar has several gurus working amongst its ranks, and its services are backed by CI financial (the biggest independent asset management firm in Canada). On top of that, they are a full-life insurance proxy in Ontario and British Colombia.

There are other bits and pieces of information you will need to know about WealthBar before deciding if they are worth the trouble.

I’ve outlined the major points here as to why people opt for WealthBar:

1. Besides their investment service, WealthBar also offers unlimited financial planning and advice to every client, regardless of their portfolio value. Every WealthBar account holder has a dedicated financial adviser. There is also a financial planning tool for investors to run different investment scenarios that will help you reach your financial goal

2. They offer more account types to residents of Quebec than most other Robo-advisors

3. While they have set ETFs for your investment needs, you also have the choice to custom-build your own investment portfolio

4. WealthBar Minimum – The minimum amount for investing with WealthBar stands at the low price of $1000. If you do not have that much, you can pay into your WealthBar account in installments until you reach the minimum amount. WealthBar will not invest your money into any of your chosen ETFs until you have at least $1000

5. WealthBar’s investment management strategy keeps your portfolio within sight of your financial goals by automatically rebalancing it should it tilt more than 5% from your allocated objective

6. This one is not exclusive to WealthBar, but your investment is secured by CIPF and IIROC via the independent custodian’s BBS, Credential Securities, and NBIN. This means that all your funds in WealthBar are insured up to $1 million for every account type you hold in the event that WealthBar goes bankrupt and folds

7. WealthBar offers a risk-free trial period after which you can also leave at no cost if you find it is not a good fit

8. If you are transferring your investment to WealthBar from another broker, WealthBar will rebate your transfer fees up to $150 for transfers of $25,000 and above

9. WealthBar also offers many other services like tax optimization, insurance needs analysis, corporate tax planning, and estate planning among others.

WealthBar Performance Over The Years

Based in Vancouver, WealthBar was launched in 2014 – Canada’s first full-service Robo-advisor – by a husband and wife team, Chris and Tea Nicola. Both have a wealth of experience in financial advisory and wealth management. In addition to his time working for his father’s wealth management company, Nicola Wealth, Chris also has extensive experience as a software and web developer.

After managing the wealth of affluent Canadians for so long, Tea and Chris decided to launch a Robo-advisor to make the same exclusive private investment opportunities of the wealthy 1 percent available for the 99 percent. Unlike most other brokerages and Robo-advisors, WealthBar is also very transparent in their approach: since their inception, they have always posted the performance of their portfolios online for the world to see and the view has been impressive.

So with exclusive private portfolio opportunities and asset classes, transparency, and also low fees investing, what else is there to say about them? This WealthBar review will give an overview of the Robo-advisors investing and trading products, performance, types of portfolios, and so on. This will help you recognize if WealthBar is the right fit for your investment objectives.

WealthBar Account Types

WealthBar Account Types

The ultimate reason for investing will always differ between investors. While some want to grow their long term savings free of taxation, others are garnering finance to live off during retirement, while some others are saving up capital to start their business venture and so on.

Whatever the case, you will likely find a type of investment account that fits your particular needs among WealthBar’s plethora of account options. Here are some of the major account types available:

1. RRSP (Registered Retirement Savings Plan). This is simply a tax-advantaged method of saving up for your retirement. Profits from investments held in an RRSP are tax-free and only withdrawals are taxed. It can be opened individually, by a couple, or by a group.

2. TFSA (Tax-Free savings account). This works just like the RRSP but is leveraged for more general savings purposes and can go on forever

3. RESP (Registered Education Savings Plan). This account type is perfect for parents who want to keep putting away (and investing) some money for their kid’s education after secondary school. Contributions to the account are tax-free and can also be matched by some government grants

4. RDSP (Registered Disability Savings Plan). This one is geared towards making funds available to cater for people with various kinds of disabilities. Disability tax-credit eligible users here can also benefit from additional gains contributed to their RSDP from various bonds and government grants

5. RRIF (Registered Retirement Income Fund). An RRSP account is converted into an RRIF account once the holder has retired and is ready to start taking withdrawals from their RRSP

6. LIRA (Locked-In Retirement Account). This holds and locks pension funds for investors who were former members of a pension plan

7. LIF (Life Income Fund). Like the RRSP/RRIF relationship, the LIF is the account used to take regular withdrawals from a LIRA account

8. Non-registered investment accounts. These accounts are more general in their investing scope and have much higher limits than an RRSP or TFSA. It can also be used to invest by Canadians who are living/working outside the country

9. Corporate/Business investment accounts. Perfect for investors who want to operate their investments under a business name

10. IPP (Individual Pension Plan). More or less an alternative to the RRSP with a focus on executives and business owners

WealthBar Investment Portfolios

This Robo-advisor is known for its many carefully chosen ETFs on offer. Fees for investing in these ETFs are low and naturally, investment growth depends on your risk profile and tolerance, and investment goals. WealthBar uses this information to select the best portfolios for you to invest in.

The portfolios available via WealthBar are categorized such that the investment risk for each portfolio is directly proportional to its reward/growth.

1. WealthBar Aggressive ETF Portfolio – Maximum growth possibility with high volatility. This portfolio is made up of 5% preferred shares, 10% real estate, 22.5% bonds, 62.5% equities

2. WealthBar Growth ETF Portfolio – Focused on growth with moderate volatility. The portfolio comprises 32.5% bonds, 52.5% equities, and a 15% mixture of real estate and preferred shares

3. WealthBar Balanced ETF Portfolio – Moderate growth and moderate volatility. This ETF portfolio is made of 41% bonds, 44% equities, and a 15% real estate and preferred shares

4. WealthBar Conservative ETF Portfolio – Mainly focused on investment protection and steady growth. Low volatility. The portfolio is 56% bonds, 29% equities, and 15% real estate and preferred shares

5. WealthBar Safety ETF Portfolio – Solely designed for investment presentation and protection. Little to no volatility. The portfolio contains 69% bonds, 16 percent equities, and 15% real estate and preferred shares

As can be seen, the WealthBar Aggressive Portfolio is for those with the highest risk tolerance, while the Safety ETF portfolio is for those who want guaranteed investment protection regardless of growth rate.

For each of these portfolios, WealthBar has strategically chosen a list of 8 to 10 ETFs to make them up.

All the chosen ETFs keep to WealthBar’s low-cost investment strategy and are gotten from ETF providers like iShares, BMO, Vanguard, Horizon, and Purpose among others.

These ETFs include:

-

Purpose High-Interest Savings ETF (PSA)

-

iShares Core MSCI EAFE IMI ETF (XEF)

-

Vanguard Canadian Short-Term Corp Bd ETF (VSC)

-

Horizons S&P/TSX 60 ETF (HXT)

-

And more

Also, for the socially responsible investors, WealthBar also gives investors the opportunity to purchase the environmentally friendly ETF, Invesco Cleantech ETF (PZD), as part of their investment portfolio. WealthBar only allows you to commit 5% of your portfolio to Cleantech though. It also helps that Cleantech has a proven record of impressive performance.

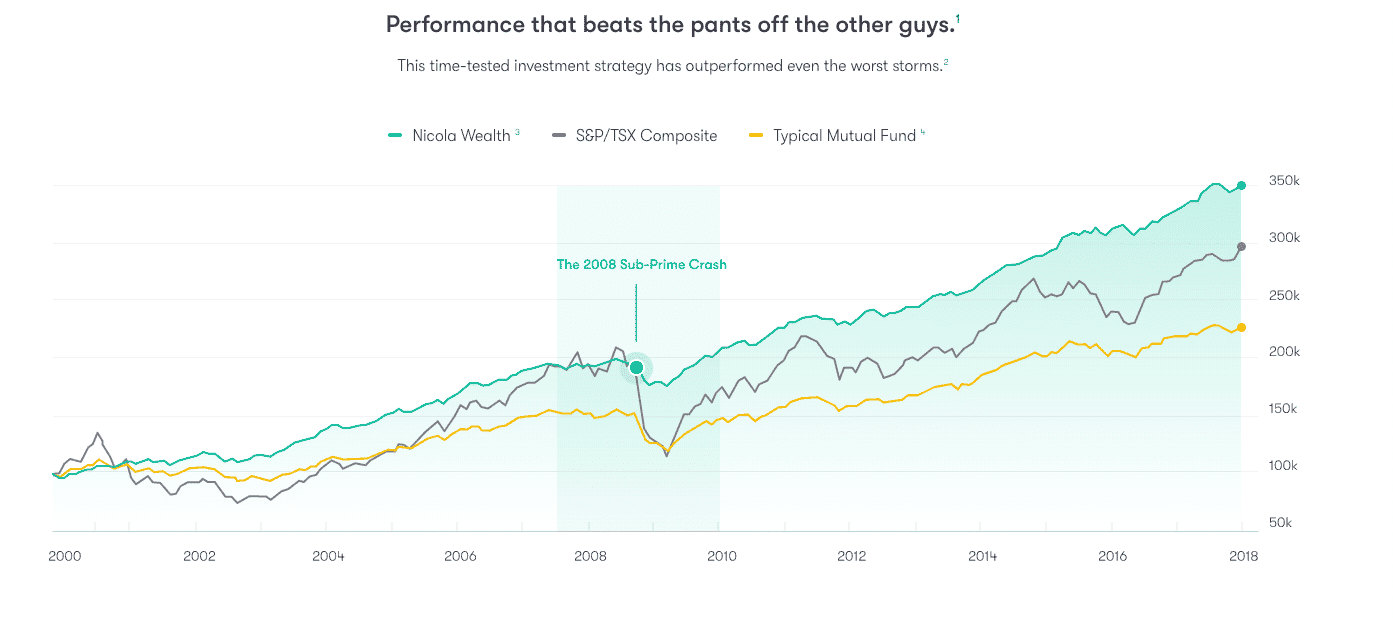

WealthBar’s Private Investment Portfolios

And then there’s WealthBar’s exclusive private investment portfolio. These portfolios are offered to WealthBar’s users from Chris Nicole’s father’s portfolio management company, Nicola Wealth. The company bought a majority stake in WealthBar through via CI Financial’s acquisition in 2018, giving WealthBar access to these exclusive investment opportunities.

These private portfolios are also known as “all-weather portfolios” and are designed for growth, regardless of the market conditions at any given time. Such investment opportunities are usually exclusively privy to wealthy investors with millions to invest.

Thanks to WealthBar’s relationship with Nicola Wealth, low-budget investors in Canada can add these portfolios to their investments.

What Are The Fees Associated With WealthBar’s Services?

And now we come to the fees, one of the most attractive features of WealthBar. Unlike most other brokerages and Robo-advisors, WealthBar’s fees follow a multi-tiered pricing system where the fee paid by investors is a predetermined percentage of their investment amount.

First of all, it’s nice to know that WealthBar will manage your investment at no cost if your portfolio value is below $5000. The fees paid for higher amounts are stated this:

-

From $5001 – $149,999: 0.6% annual fee rate

-

From $150,000 – $499,999: 0.4% annual fee rate

-

For $500,000 and above: 0.35% annual fee rate

These are the only fees you’ll ever pay to WealthBar and this covers all the services you get from them from financial planning efforts to managing and trading your portfolio.

This fee structure does not mean that you will pay a fee of 0.35% if you only have $500,000 in portfolio value. Your investment will instead be broken down into firsts. So for a $500,000 investment, the first $150,000 will be charged at 0.6%, leaving $350,000 which can then be charged at the corresponding rate of 0.4%.

WealthBar Vs. Wealthsimple

While WealthBar ETF investment is significantly less costly than trading mutual funds with a traditional brokerage, you may be able to get lower fees from other online brokerages and Robo-advisors such as Wealthsimple.

Wealthsimple’s fee structure is simpler to understand. Users pay a 0.5% annual rate for a portfolio value below $100,000 and 0.4% annual rate for a portfolio value above $100,000.

A $90,000 investment will cost you a management fee of:

-

$540/year with WealthBar

-

$450/year with Wealthsimple

While an investment of $500,000 will cost you:

-

$2300/year with WealthBar

-

$2000/year with Wealthsimple

These fees are still pretty close are much better than traditional mutual funds investing that will set you back around $1980 for a $90,000 investment and a dizzying $11,000 for a $500k portfolio.

In addition to these fees, there is also an MER fee that is built into your fee structure but is not displayed like WealthBar’s management fees. The MER fees go anywhere from 0.29% to 0.35%. The particular fee is paid directly to the providers of the ETFs you are invested in.

For WealthBar’s private investment portfolios, the MER is even higher (at around 1.56%). This is still lower than the average fees for traditional mutual funds though.

While fees are a strong point for deciding which Robo-advisor to opt for, you also have to check out the features and services of each one. You may find that the one that is slightly costlier is the one that has all the features and provides all the services you need for your investing.

Wealthsimple Halal Investment

Wealthsimple’s Halal Investing portfolio is a simple and low-cost way to grow your money. Your portfolio is optimized not only for performance but for companies and investments that comply with Islamic law.

Key Features Of Wealthsimple’s Halal Investment

1. All Halal investments are screened by a third-party committee of Shariah scholars.

2. No Halal investment in companies that profit from gambling, arms, tobacco, or other restricted industries

3. No businesses that derive significant income from interest on Halal loans

Pros of using Wealthbar

- Wide-ranging portfolio

A standout among the long list of advantages that wealthbar offers over other similar Robo-advisor platforms in Canada and beyond is that they over a much-diversified portfolio. In general, wealthbar offers 5 different ETF portfolios.

With every ETF portfolio offered on their platform, they include another 8-10 separate low-fee ETFs from well-renowned providers such as Purpose, BMO, Horizon, iShares, and vanguard. Thus, giving customers a long list of options to choose from regardless of their financial capacity.

- Custom Financial advice:

Personalized services are hard to come by when it comes to professional investment management, and as such, many investors appreciate the effort that Wealthbar puts into creating portfolios that match their needs perfectly.

Wealthbar makes it a point to provide investors with dedicated financial advisers to provide the necessary assistance when the need arises.

- No extra Charges

Whereas it is common to incur extra service costs following the originally stipulated charges of a stock portfolio when investing with conventional investment management companies, Wealthbar begs the difference.

Wealthbar will never ask you to pay extra fees on an account unless such a fee was stipulated from the get-go.

- Automated Rebalancing of portfolio

Another thing you’ll come to love about this Canadian fin-tech pioneering firm is that it helps investors rebalance their portfolios when they deviate a little over five percent from the target allocation.

In this way, protecting investors from hurtful losses on their accounts.

- Secured

When it comes to internet-based investment management companies and Robo-advisor, in general, the main area of concern is the safety of the funds invested. Besides, no one wants to lose money on a stock portfolio, at least not to a fraudulent advisor.

With Wealthbar guiding your investment activities, you can invest your funds with both eyes closed. It is also worth mentioning that the Wealthbar is backed by CI financial and they belong to the CIPF and IIROC group.

- Offers SRI

Wealthbar is committed to providing investment portfolio opportunities that align well with the investor’s beliefs and values. On top of that, they provide stock portfolios options that are advantageous to the environment via the Cleantech portfolio.

With all these exclusive portfolio choices and investment advice opportunities, it would seem like Wealthbar is the perfect Robo-advisor for all your financial management activities. Maybe it is.

However, there are a few grey areas in their services that you need to consider before choosing the WealthBar as your Robo advisor.

Cons Of WealthBar

Maintenance fee more than the industry average

The only snag to Wealthbar’s near-perfect investment management services is that they demand a 0.85% service fee from account holders. Whereas this is not the highest we have seen in the Robo investment industry, it may add up long term.

Conclusion

If you want mutual fund-type investing but do not have the funds for it, WealthBar helps affords to invest in private portfolios that are usually the domain of the high-net-worth investors. There’s also the part about the low fees, low minimum investment of $1000, and the human financial advice included in every investor’s package.

With over $250 million in assets under management and the backing of their parent company, Nicola Wealth, they apparently are doing something right.

However, all these do not mean that WealthBar is the best (or not the best) Robo-advisor in Canada. Still, if you have very particular needs from your Robo-advisor, like looking for the lowest fees, then other options like Wealthsimple will give you lower fees overall, especially if you have a large budget above $100k.

With over 40 years’ worth of fin-tech experience backing the Wealthbar Robo-advisor company, it is the ideal investment manager to handle your portfolios and provide professional financial advice for your assets.